")

Written by Gregory S Mathew

Blockchain, the underlying technology behind the sensational Bitcoin, could profoundly impact the Oil and Gas industry by cutting down on operational time and costs while also introducing more transparency to the industry. The technology recently garnered headlines when a group of seven oil companies, including American giants like ExxonMobil and Chevron, agreed to form the first industry blockchain consortium, according to a press release. The consortium aims to explore the potential benefits that blockchain technology can deliver to the space.

This article will explore the potential use-cases and benefits blockchain technology could deliver to the Oil and Gas industry, while also mentioning the market trends.

Interestingly, Industry giants like ExxonMobil are not alone in exploring the potential use cases of blockchain in the Energy sector, instead, they are partnering startups like Vakt, which is a digital ecosystem for physical post-trade processing. Startups like Vakt, that aim to mitigate some of the problems in the energy sector using blockchain technology have raised a whopping $490 million till date (source). Before we dive into how blockchain technology can help revamp the Oil and Gas sector its important to understand what blockchain technology is.

The bare bones of blockchain technology

In essence, blockchain is an immutable digital ledger of economic transactions, that is secured through cryptographic methods and can be programmed to record the transaction of anything of value. The blockchain is monikered so because the information is stored in ‘blocks’ on a ‘chain’ but not in the physical sense. One of the inherent qualities of a Blockchain network is that it is decentralized, meaning it is not owned by a single entity, instead a network of computers (nodes) makes up a blockchain network.

How does this network of computers help introduce more security and transparency? The answer to that question lies with how information gets updated on a blockchain network.

Transactional information like participants involved, the value transferred and specific details of the transactions are stored in ‘Blocks’ on a blockchain network and each ‘Block’ can store up to several hundred transactions. Although storing transactional data on a decentralized network might seem counter-intuitive to increasing security but this is where cryptography comes into play, as all the data is encrypted. Once a Block has been hashed, which means all transactions on that block have been verified (by nodes) and the block itself has been assigned a unique identification code, the block is added to the blockchain.

Once a block has been added to the blockchain, it’s incredibly difficult to tamper with it, as the information is periodically verified across all nodes on the network. If the data is manipulated in a few nodes, the remaining nodes pick up the discrepancy. Which means any data manipulation would require control over at least 51% of the nodes, which is extremely difficult on a sufficiently large blockchain network.

Challenges faced by the Oil and Gas industry

To digress, the industry may be going through its most challenging time yet as countries the world over try to reduce their carbon emissions to comply with global emission norms like the Paris Accords, which has led to a polarizing debate of renewable energy versus fossil fuels. But coming back to the topic of this article, the industry still uses outdated platforms to trade energy resources and employs less-than-secure documentation method that is highly susceptible to security threats, while also being prone to human error. Here are some of the back office challenges that the Oil and Gas industry is suffering from-

- Energy transactions often involve a wide range of documents and orders such as purchase invoices, shipping documents, bank release funds etc which adds to the complexity of the process.

- For industry giants like ExxonMobil making sure all documents are in place and accessible to all stakeholders, is a time-intensive process. These documents can include compliant documents, audits, and associated paperwork.

- The supply chain network for large oil companies is incredibly complex, involving various parties such as shippers, suppliers, and customers on a global scale.

- Oil and Gas contracts often ordain cross-border payments, which makes the payment structure complex as cross-border payments are time-intensive and incur additional costs.

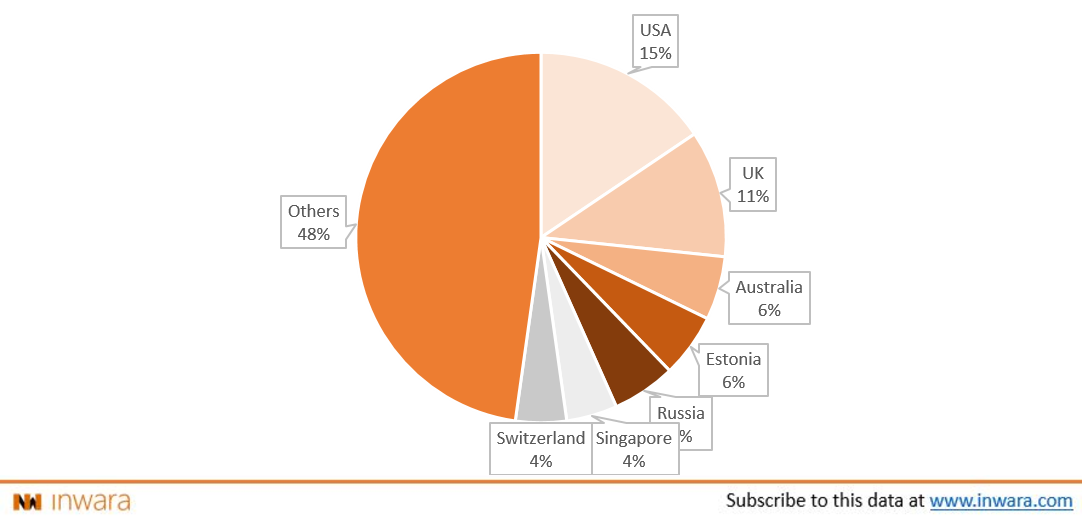

To mitigate these issues many “Energy sector” startups have popped up over the years but a surprising number of these were from the United States of America.

A whopping 15% of the total number of Energy based Blockchain-crypto projects in the world are from the US. But this comes as no surprise when considering the fact that the USA has become the world’s largest exporter of crude oil, surpassing countries such as Russia and Saudi Arabia.

7 use cases for Blockchain technology in the Oil and Gas industry

Blockchain technology can help mitigate several of these back-office problems as it embeds trust into the very nature of transactions. With blockchain technology, all parties involved could likely use an established, distributed network of computers that keep track of every economic transaction on the network.

Oil and gas companies will likely use a private blockchain network, which is different from the public blockchain networks used in the case of Bitcoin and other cryptocurrencies. In essence, a private blockchain only allows invited parties or nodes to view the data on transactions, the polar opposite of these are public blockchains like that of Bitcoin where the transactional information can be viewed by literally anyone with an internet connection. This means that a private blockchain can boost trust among various parties within the industry from suppliers to shippers, while still being secure from outside parties.

With that being said, let’s consider the potential use cases and benefits of a private blockchain network in the Oil and Gas industry-

- #1: Crude oil transactions could be digitized– Using blockchain, crude oil transactions can be digitized that ensures enhanced security, improved transparency and optimized efficiency. Natixis, a French corporate and investment bank was the first to pioneer a blockchain solution in commodity trade for US crude oil transactions.

As all trading parties including buyer and seller along with their respective banks are on the same distributed ledger. All details pertaining to the transaction is simultaneously visible to everyone that increases transparency in the process. This step could also reduce the threat due to fraud and cybercrime because of the distributed nature of blockchain while at the same time reducing overhead costs, cash cycle times and cost intermediaries.

- #2: Improved trust among parties in the industry- A private blockchain network could safely store the track record of employee and contractor certifications (H2S training, first aid, welding, etc). On top of boosting trust between companies and contractors/ employees, such a blockchain network could also help cut down on hiring costs while ensuring improved job safety and performance.

- #3: A cryptocurrency pegged against Oil- With oil being one the most valuable non-renewable energy sources in the world, a cryptocurrency pegged to it could be a viable replacement to traditional financial transactions. On top of this, such a cryptocurrency could enable direct transfer of value between various parties in the industry without the need for a trusted intermediary like a bank.

- #4: Augmented compliance– The Oil and Gas industry is among the most heavily regulated in the world with protocols deriving from various regulatory authorities from environmental to taxation. Regulatory authorities will be able to maximize visibility in the industry as all the transactional data is stored on a blockchain network which can be accessed in real time.

- #5: Enhanced land record management- It is critical for Oil and gas companies to properly manage land sale records which represent millions of dollars worth investments. The traditional process of maintaining such a record is cumbersome and is prone to forgery and other illicit activities. Such an important piece of documentation could be stored on the blockchain, which can create an immutable record of land ownership, transfer and value. In Georgia and Ghana, where there are high levels of land ownership disputes, blockchain technology is being explored as a viable solution.

- #6: Improved data storage for Internet Of Things- IOT is a system of interconnected computing devices or mechanical machines that are able to transfer data over a network. The Oil and Gas industry relies heavily on IOT to devices to monitor operations and increase their efficiency. But the catch is, current IOT models depend on centralized models of communication like a server/ client model. Despite being in close proximity with each other, these IoT devices have to transfer data over the internet and heavily depends on centralized storage solutions which could be at risk of cyber attacks.

An elegant solution to this is to introduce blockchain, which can distribute the computational power needed over a network of computers instead of a central computer. Due to the decentralized nature of the network, data stored will also be less likely to succumb to cyber attacks. - #7: Hydrocarbon tracking– blockchain technology can be used to track regulated substances effectively at each stage of the supply chain process. This can help improve accountability in the industry.

While blockchain technology could significantly improve the operation efficiency of the Oil and gas industry by enhancing trust among parties and enabling more transparent transactions at each stage of the process, it is not the panacea for all of the problems plaguing the industry. But the numerous benefits it could provide are significant enough to assume that integrating blockchain technology into the current Oil and Gas ecosystem seems like the rational step forward for the industry.